COVID-19, lockdown, working from home and self-isolation are now well established across the financial industry, but how are compliance teams impacted? During our recent online panel about Market Abuse Monitoring, we hosted 80 market participants from the buy- and sell-side, many from compliance and operations functions, and took the opportunity to ask them.

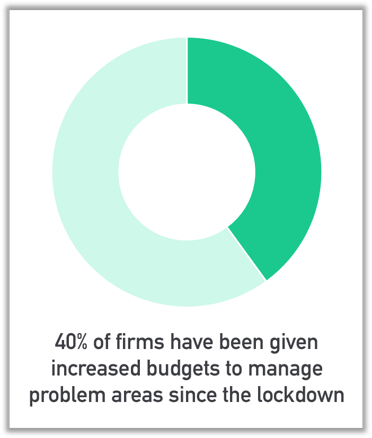

Most notably, 40% of those who took part in our  poll said that their compliance departments have been given increased budgets to manage problem areas since the lockdown. Not only is this a clear sign of the challenges presented by remote working at this scale, but it demonstrates an admirably speedy response by firms, who quickly realised that a clear focus on compliance and oversight remains essential.

poll said that their compliance departments have been given increased budgets to manage problem areas since the lockdown. Not only is this a clear sign of the challenges presented by remote working at this scale, but it demonstrates an admirably speedy response by firms, who quickly realised that a clear focus on compliance and oversight remains essential.

In a blog a few weeks ago, Helen Bevis highlighted that during this pandemic, senior managers need to adapt, yet still ensure that their regulatory processes and procedures enable them to stay on top of their obligations. This may include a complete review of internal systems and workflows to ensure they are fit for purpose for a remote workforce. Being able to access new services and technologies play an important role in managing this, and it is encouraging that our latest finding confirm that compliance managers are taking this seriously.

Unsurprisingly, our respondents also told us that monitoring communications is the most significant challenge they are facing in lockdown, and this has been the focus of the budget increase. Mobile communication and voice surveillance combined are the biggest concerns, understandable when you consider that employees are working at home, possibly using personal devices and are not always connected to firm-wide monitoring tools.

Key to monitoring communications, is the ability to overlay multiple forms of communication together for better analysis, and 50% of respondents highlighted this as the area where they are struggling.

Another key concern (with 46% highlighting this) is reactive rather than proactive alerts, which reduce the effectiveness and timeliness of compliance teams being able to review and respond to potential breeches.

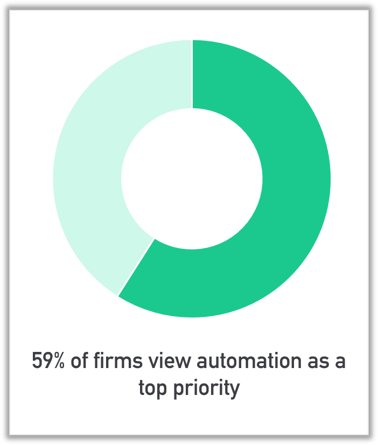

Resolving these challenges means that 59% of our respondents see automation as their top priority from a surveillance perspective.

Creating customised, automated searches with smart algorithms generates specific, timely alerts that help to identify and resolve risks quickly. Apply machine learning or artificial intelligence to this, and your surveillance system will be able to improve the accuracy of your alerts over time, based on the ones you reject or accept.

For compliance managers overseeing a dispersed workforce, this level of automation is naturally an appealing way to ensure compliance and effectively monitor your trading operations.

In addition, consolidation and normalisation of data continues to be a key focus, with 48% highlighting this as a top surveillance priority. This is an ongoing requirement that supports clients when meeting regulatory requirements and has the added advantage of driving enhanced performance insight for businesses through indexed, searchable and instantly retrievable data.

This survey was carried out during SteelEye’s recent Virtual Regs & Eggs - Expert Market Abuse Monitoring Panel which looked at the increasing need for market abuse surveillance, and the challenges faced by trading firms. These challenges have been magnified due to COVID-19, making it more difficult for firms to capture the data required for surveillance (including trades, orders, voice calls, instant messages, WhatsApp, SMS, and even things like CRM data and meeting minutes). Panellists included Haider Mannan, Data Consultant at SIX, Jon Carp, Co-Founder of Finceler8, and Nick Fulton, Capital Markets Consultant at Baringa, and was moderated by Matt Smith, CEO of SteelEye. Note, the number of respondents to the poll questions ranged from 29-34.